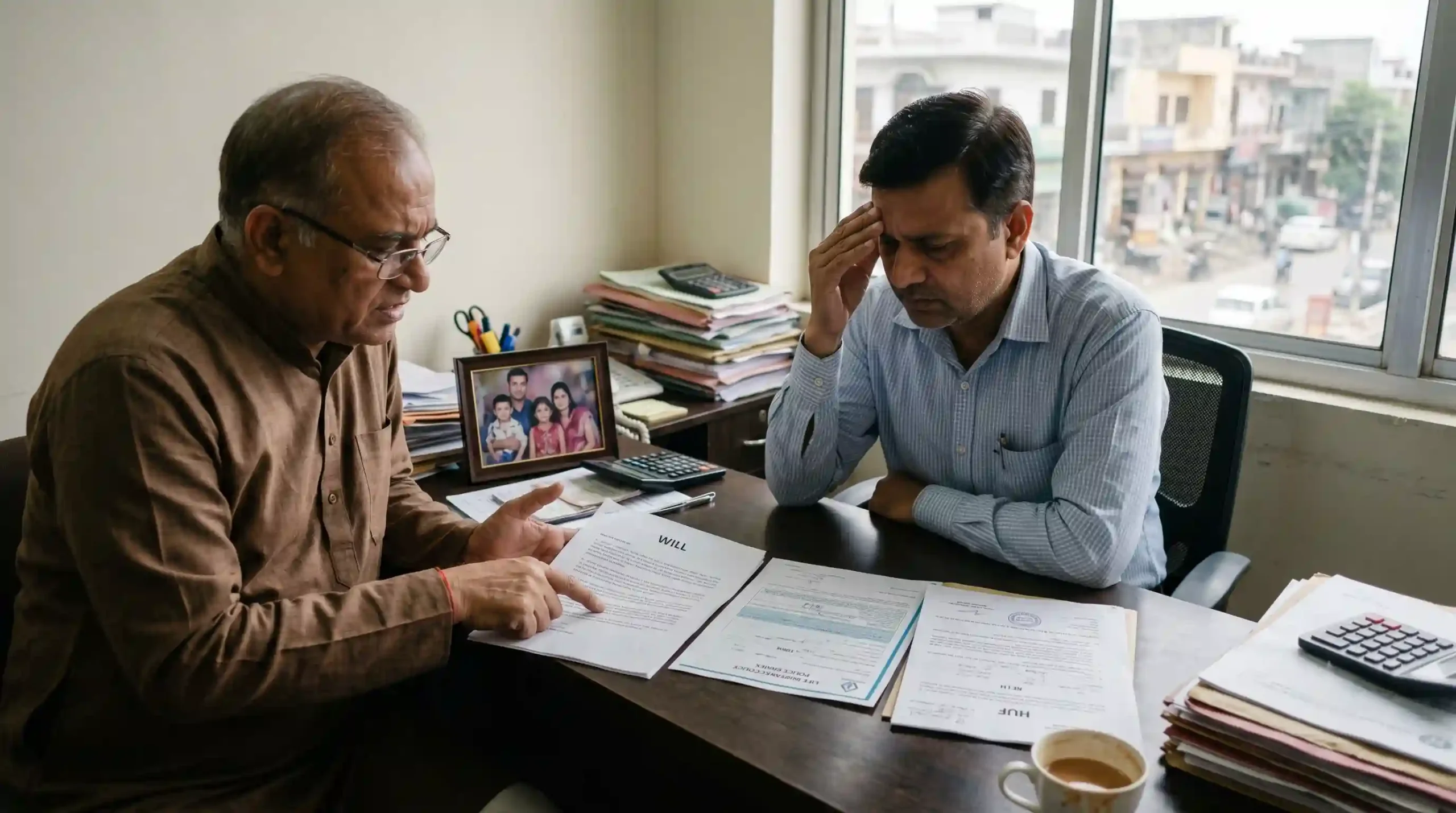

Lottery winnings insurance and estate protection India is what keeps a windfall in the family. See the two covers and one document winners set up first.

When you suddenly get a large amount of money, your biggest risks change entirely. Instead of worrying about earning cash, you must worry about losing it. Medical emergencies, sudden death, or fierce legal fights can drain your accounts quickly. Therefore, you cannot simply leave crores sitting in a bank and hope your family figures it out later.

Before you fully execute your lump sum windfall investment plan in India , you must protect your assets. Building a strong legal and medical wall around your new money is absolutely vital to ensuring multi-generational wealth.

Key Takeaways

- The Medical Shield: A severe illness can drain a windfall very rapidly. Comprehensive health insurance locks down your core cash.

- The Liability Barrier: Term insurance windfall protection replaces future taxes and creates instant cash for your family.

- The Ultimate Rule: A legally registered Will stops angry family fights and completely bypasses the slow Indian court system.

- Nominee vs. Legal Heir: Understanding complex will and nominee rules is mandatory. A nominee simply acts as a temporary holder, not the true owner.

- Expert Help: Always use a registered advisor and a good lawyer to draft these critical documents safely.

Why Lottery Winnings Insurance and Estate Protection India is Mandatory

Many new winners falsely believe that having massive cash means they do not need insurance. However, this is a very dangerous financial mistake. Proper asset protection strategies do not use insurance to make money. Instead, they use it to strongly defend the main prize money from biological and legal disasters.

If you are currently researching what to do after winning lottery in India , locking down your estate must be your first step.

To avoid fake schemes, you must always verify your insurance providers directly through the official Insurance Regulatory and Development Authority of India (IRDAI) website. ### Policy 1: Comprehensive Global Health Insurance

First, you might wonder why you should buy health insurance when you have ₹1 Crore in the bank. Simply put, a severe medical crisis can easily cost over ₹50 Lakhs today.

If you pay out of your own pocket, you must break your investments early. This immediately triggers massive capital gains taxes. Ultimately, paying cash for medical bills permanently shrinks your long-term wealth.

Therefore, a premium health insurance policy acts as a strong financial shield. It absorbs the shock of high medical bills. As a result, your primary windfall remains completely untouched and keeps compounding.

Policy 2: Term Insurance Windfall Protection

Second, many winners wonder if term insurance remains necessary once they get rich. The answer is clearly yes. When you win, your family’s daily lifestyle inflates immediately.

If you pass away suddenly, transferring your investments to your heirs can take years. However, term insurance provides an instant, tax-free cash payout directly to your family within weeks.

This fast cash easily covers any sudden taxes or legal fees. Furthermore, it pays for their daily living costs while your main assets are slowly untangled in probate court.

Drafting the Document: Will and Nominee Rules

Insurance safely protects your money while you live. Conversely, a Registered Will protects your family after you die. Estate planning in India involves very strict laws. Relying on default rules guarantees a major disaster.

You must clearly understand the difference between a will and nominee rules. When you open a bank account, you name a nominee. However, under Indian law, a nominee is merely a custodian. They are legally forced to give the money to your true legal heirs.

Combining Trusts with Lottery Winnings Insurance and Estate Protection India

If you die without a Will, your massive windfall gets divided by rigid religious laws. This instantly triggers angry family fights, frozen bank accounts, and long court battles.

To avoid this nightmare, explicitly write down who gets what. Additionally, pair your Will with a strong HUF trust structure lottery winning tax plan.

This advanced lottery winnings insurance and estate protection India step ensures your assets skip probate courts completely. It transfers your wealth to the next generation safely without heavy taxes or public family wars.

Disclaimer: This article provides general financial and educational information, not formal legal or tax advice. Always consult a certified legal professional and a SEBI-registered investment advisor regarding estate planning and insurance structures.

Frequently Asked Questions

How do I protect a lottery windfall for my family?

First, you protect it by immediately setting up a strong estate plan. This involves drafting a legally registered Will. Next, you must purchase high-cover global health insurance to prevent medical bankruptcy. Finally, set up term life insurance to give instant cash to your family.

Do I need life insurance after winning the lottery?

Yes, term life insurance remains highly critical. Even though you possess immense wealth, transferring those assets after death can take years. Therefore, a term policy delivers an instant, tax-free cash payout so your family survives the waiting period comfortably.

What is the role of health insurance after a windfall?

Health insurance acts exactly like a financial wall. Instead of selling your good mutual funds and paying heavy taxes to fund a medical emergency, the insurance company pays the bill. Consequently, this leaves your wealth engine completely intact.

Should I write a will immediately after winning?

Absolutely. Drafting and registering a Will must happen within the first 30 days of claiming your prize. Without it, your newly acquired millions fall under default religious laws. Ultimately, this practically guarantees vicious legal battles among your extended family.

How does estate planning protect lottery winnings?

Estate planning uses legal tools like Private Family Trusts and Wills to dictate exact ownership. Furthermore, it legally shields your assets from future creditors. It also lowers taxes during wealth transfer and blocks extended relatives from taking your prize.

What happens to lottery money if a winner dies without a will?

If you die without a Will, the Indian legal system freezes your assets immediately. The courts will distribute your winnings based on specific religious acts. Consequently, this painfully slow process tears families apart and drains the estate through endless legal fees.

Can a nominee claim my investments automatically?

A nominee can claim the funds from the bank easily, but they do not legally own the money. Under Indian law, a nominee acts strictly as a trustee. Therefore, they are legally forced to distribute those funds exclusively to your defined legal heirs.

How do I shield assets from disputes after a windfall?

The best defense involves moving your core investments into a Private Family Trust. A trust acts as a separate legal entity, meaning the assets no longer belong to you. Effectively, this blocks angry relatives or silly lawsuits from touching your capital.

Is term insurance still worth it for a crorepati?

Yes. Term insurance is extremely cheap compared to the massive cover it provides. For a crorepati, it serves as an instant cash tool. It pays off any outstanding debts or estate taxes immediately. As a result, your actual investment portfolio stays safe.

What documents protect a sudden fortune in India?

You immediately require three specific documents. First, get a legally registered Will. Second, create an updated Nominee Declaration across all bank accounts. Finally, you should optionally draft a Private Trust Deed for absolute asset protection.