Reviewed for Accuracy by: Tax Compliance Editorial Board

Disclaimer: This article provides informational context regarding windfall tax compliance under the current income tax framework. It does not constitute formal legal or financial advice. Taxpayers must consult a qualified cross-border tax expert or verify rules against the latest Finance Act provisions before filing.

Celebrating a major windfall from an Indian lottery or sweepstakes can be life-changing, but relying solely on the platform’s initial deduction is a critical mistake. Many high-value winners view Tax Deducted at Source (TDS) as a final settlement, completely unaware that they must manually calculate and pay advance tax on lottery winnings to avoid severe compliance penalties.

Therefore, analyzing your true liabilities under the current fiscal year mandates is the only way to safeguard your wealth. This processing system operates under strict automated clearing parameters.

To understand how automated withholdings tie into the overarching master tax code, review our definitive guide on Lottery Tax in India. Failing to clear the resulting shortfall before the quarterly financial deadlines can lead to sudden, systemic bank account freezes.

📌 Key Takeaways

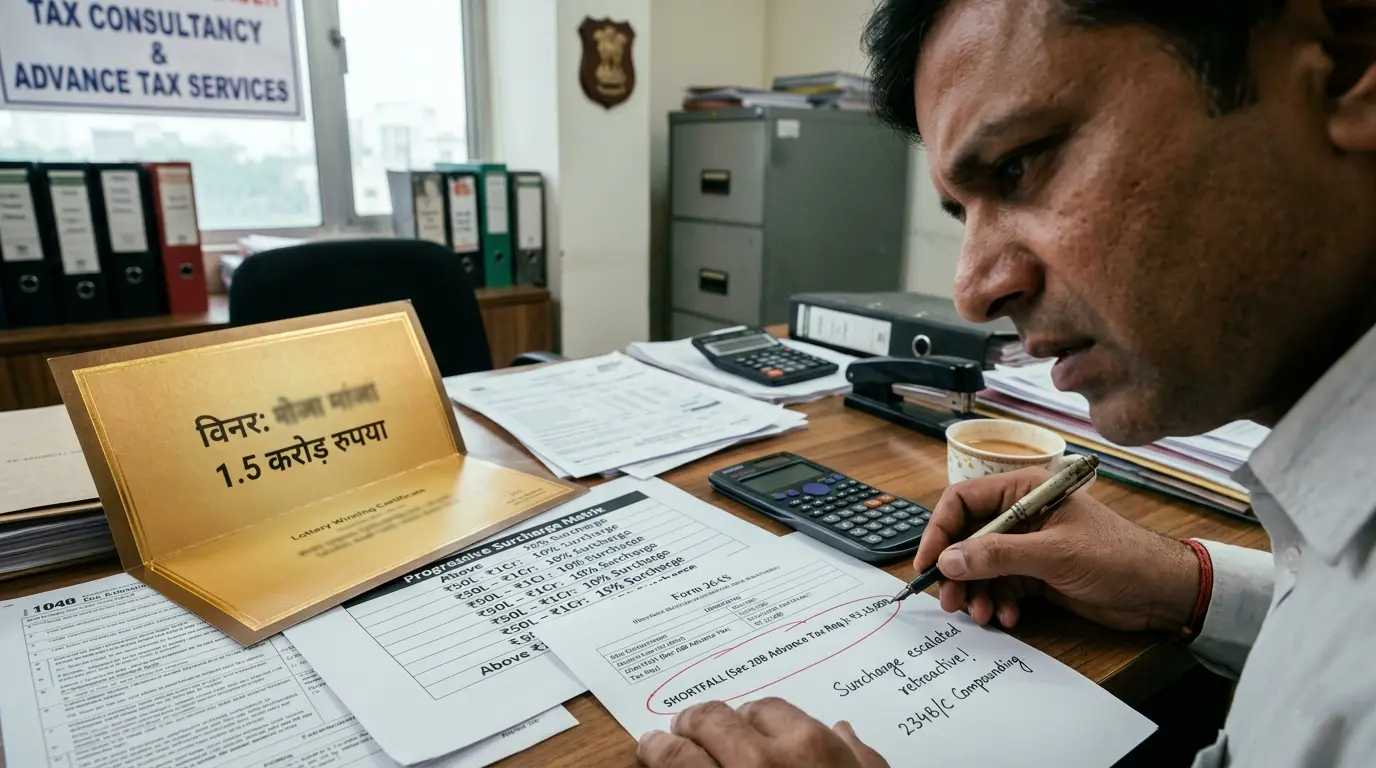

- Provisional Credit Only: First, the 31.2% withholding executed by lottery platforms is merely an interim payment, not a final tax clearance.

- The Surcharge Factor: Furthermore, your combined annual salary, business profits, and investments can retroactively push your windfall into higher surcharge brackets.

- Immediate Deadlines: Section 208 mandates immediate advance tax payments if your residual tax liability after subtracting TDS credits exceeds ₹10,000.

- Compounding Interest: In addition, ignoring the remaining tax gap results in automated interest penalties under Sections 234B and 234C.

The Mechanics of Lottery TDS vs. Total Liability

The Indian tax framework sets clear boundaries between withholding rules at the source and your final reporting obligations. Primarily, the state uses this system to ensure immediate revenue collection on large prize disbursements.

Under the updated provisions of the Income-tax Act, online platforms, lottery distributors, and contest organizers must deduct tax before transferring windfall funds to a winner. Currently, this equates to a 30% flat tax plus a 4% health and education cess, establishing a baseline 31.2% TDS rate.

However, this systemic deduction is treated as a provisional credit rather than a conclusive clearance of your total tax file. The tax department evaluates your final obligations by looking at your cumulative income profile, which often exposes unexpected tax shortfalls.

Surcharge Escalations and the Need for Advance Tax on Lottery Winnings

The core vulnerability for high-earning winners stems from the progressive nature of the national surcharge matrix. While the lottery organizer calculates TDS purely on the singular prize ticket value, your final tax file aggregates all earnings.

Total Income Aggregation and Surcharge Thresholds

Your total gross income determines the surcharge slab applied to your entire tax file. If your combined salary, business gains, and windfall cross the ₹50 Lakhs threshold, a compounding surcharge kicks in retroactively:

- ₹50 Lakhs to ₹1 Crore: A strict 10% surcharge is levied directly on your base tax liability.

- ₹1 Crore to ₹2 Crores: An escalated 15% surcharge applies to your base tax calculation.

- ₹2 Crores to ₹5 Crores: The surcharge scales up significantly to 25% for high-net-worth individuals.

- Above ₹5 Crores: The peak surcharge rate reaches 37% for top-tier earners.

Because the deductor may only apply the baseline rate without factoring in your external wealth, this hidden discrepancy creates a massive funding gap in your file. Failing to calculate this compounding liability leaves you exposed to aggressive under-payment penalties. Non-resident players face an even more complex cross-border framework, which you can analyze in our guide on NRI Lottery Winnings Tax in India.

Section 208 Mandates and Advance Tax Schedules

Relying on year-end reconciliations to pay off your residual tax gap is a highly expensive mistake. The income tax framework enforces strict quarterly payment schedules that apply to all forms of taxable income.

Under Section 208, any taxpayer whose residual tax liability exceeds ₹10,000 after subtracting TDS credits must pay Advance Tax. Because a lottery win occurs as an unpredictable, sudden windfall event, it instantly triggers these advance compliance rules.

Failing to pay advance tax on lottery winnings before the quarterly deadlines causes the e-filing portal to automatically assess compounding interest penalties when you submit your return. Specifically, Section 234B and Section 234C interest charges accrue at 1% per month for delayed or skipped payments. To ensure full alignment with updated electronic payment formats and deadlines, always cross-reference your schedules with the Official Income Tax Department Portal.

Reconciling Form 26AS, AIS, and Your Final Tax File

Before attempting to file your annual returns, you must reconcile your data across multiple digital governmental ledgers to ensure absolute compliance.

Your Form 26AS ledger must show the exact TDS amount deducted by the organizer under the correct tax category. Simultaneously, the Annual Information Statement (AIS) tracks your digital banking trail to ensure the windfall amount matches perfectly.

If your prize was relatively small, you can cross-reference these logging steps with our guide on income tax on lottery winnings below 10000. When evaluating your total liability and computing the required advance tax on lottery winnings, you must ensure perfect data alignment across all forms to prevent the automated generation of mismatched compliance notices.

Frequently Asked Questions

Why do I need to pay advance tax on lottery winnings if TDS was already deducted?

TDS only covers a baseline tax rate of 31.2%. If your total annual income, including the lottery windfall, exceeds ₹50 Lakhs, progressive surcharges apply retroactively. You must pay advance tax to cover this shortfall if your residual liability exceeds ₹10,000.

What are the interest penalties for skipping advance tax on lottery winnings?

Skipping advance tax triggers interest penalties under Sections 234B and 234C. The tax department charges compounding interest at a rate of 1% per month on the unpaid tax shortfall from the deadline date until the balance is fully cleared.

How do I calculate advance tax on lottery winnings with other incomes?

You must estimate your total annual income, including salary, business profits, and the gross lottery prize. Compute the total tax and applicable surcharges, subtract the TDS already deducted, and pay the remaining balance across the standard quarterly advance tax installments.

Can I clear my lottery tax shortfall during regular ITR filing?

While you can pay the remaining balance during ITR filing, doing so will attract heavy interest penalties under Sections 234B and 234C. To avoid these extra charges, you must pay the tax via the advance tax portal during the financial year you won.

Conclusion & Next Steps

In summary, the belief that lottery TDS settles your full tax bill is a dangerous financial blind spot. While the organizer’s upfront deduction covers the baseline tax rate, your aggregated income and progressive surcharges ultimately dictate your true obligation.

Therefore, do not let your windfall slip away into avoidable interest penalties and legal fees. Review your Form 26AS ledger entries immediately, compute your true liability against the national surcharge thresholds, and clear any outstanding tax balance through the advance tax portal before the next quarterly deadline.