Reviewed for Accuracy by: Tax Compliance Editorial Board

Disclaimer: This guide provides strategic compliance insights based on the current Income-tax Act provisions. It does not constitute formal financial or legal advice. Taxpayers must consult a qualified Chartered Accountant (CA) to evaluate their specific tax profiles before filing returns.

Think a standard withholding at the source completely squares your account with the income tax department? Relying blindly on the lottery tds 10000 threshold rules is one of the quickest ways to trigger an automated compliance notice under modern tracking systems. Many casual players and high-value winners view the initial tax deduction as a final settlement, completely ignoring how secondary income streams can retroactively disrupt their tax calculations.

Therefore, analyzing your true tax profile under the current fiscal year mandates is the only way to safeguard your wealth. This processing system operates under strict automated clearing parameters.

To see how these instant withholdings tie into the overarching national tax framework, review the comprehensive Lottery Tax in India pillar page. Failing to clear the resulting shortfall before the quarterly financial deadlines can lead to sudden, systemic bank account freezes.

📌 Key Takeaways

- Provisional Nature: First, the upfront deduction triggered by the withholding limit is merely an interim credit, not a final tax clearance.

- The Surcharge Risk: Furthermore, your combined annual salary, business profits, and investments can retroactively push your windfall into higher tax brackets.

- Advance Tax Mandate: Section 208 requires immediate advance tax payments if your residual liability after TDS exceeds ₹10,000.

- Compounding Penalties: In addition, ignoring the remaining tax gap results in automated interest penalties under Sections 234B and 234C.

Understanding the Lottery TDS 10000 Threshold Mechanics

The Indian tax framework sets clear boundaries between withholding rules at the source and your final reporting obligations. Primarily, the state uses this system to ensure immediate revenue collection on large prize disbursements.

Under the updated provisions of the Income-tax Act, online platforms, lottery distributors, and contest organizers must deduct tax before transferring windfall funds to a winner. However, this rule only applies if a single prize payout crosses the statutory lottery tds 10000 threshold.

Consequently, if your winnings fall below this limit, the distributor transfers the full cash amount without any upfront deductions. If you find yourself in this situation, you can read our specialized guide on income tax on lottery winnings below 10000 to see how to manually clear your liability.

How Your Final Tax Liability Exceeds the Lottery TDS 10000 Threshold

The primary compliance hazard for high-earning winners stems from the progressive nature of the national surcharge matrix. While the payout agent calculates TDS purely on the singular ticket value, the e-filing portal aggregates your entire income profile.

Total Income Aggregation and Surcharge Thresholds

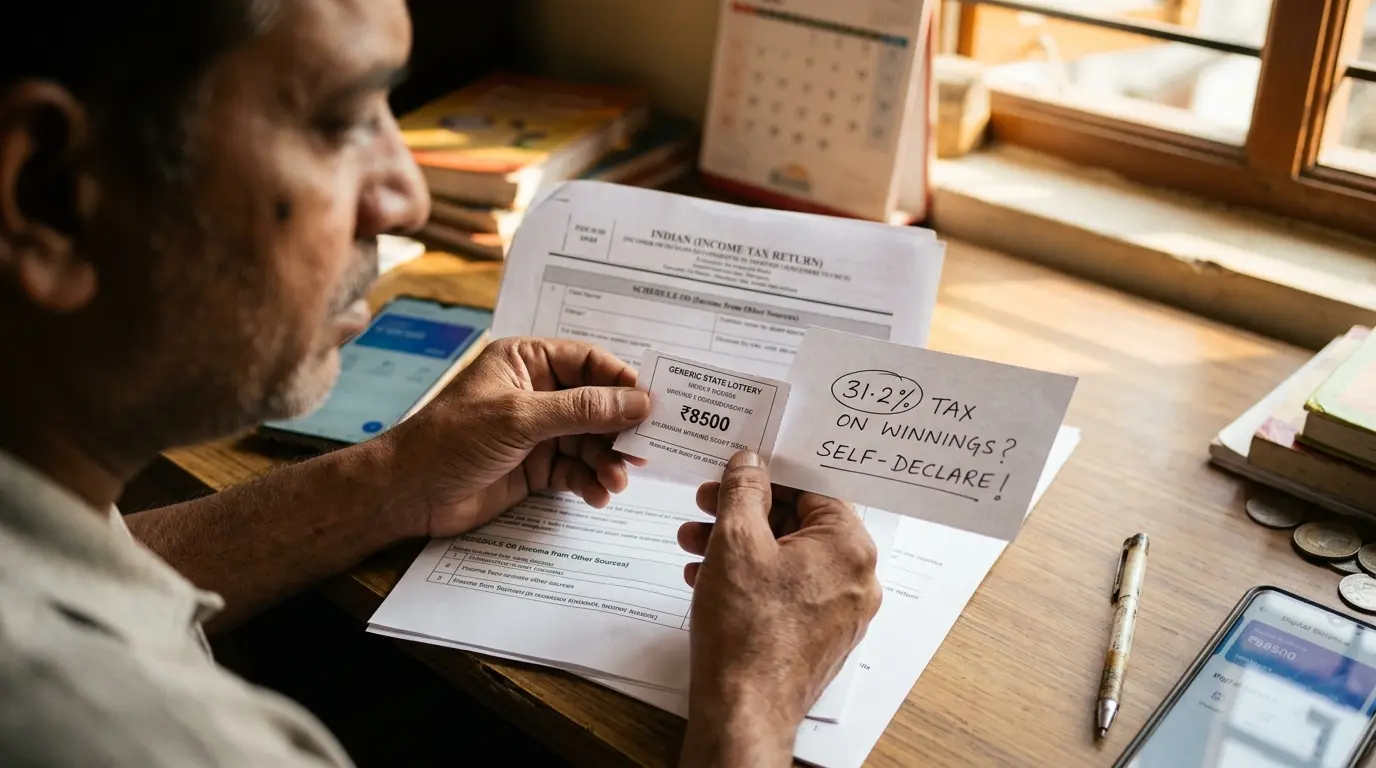

Your total gross income determines the exact surcharge slab applied to your file. Even if an online platform deducted tax upfront because your prize crossed the lottery tds 10000 threshold, they only withheld the base rate of 30% plus a 4% cess (totaling 31.2%).

If your cumulative annual income—including salaries, business gains, and your windfall—crosses the ₹50 Lakhs mark, compounding surcharges apply retroactively:

- ₹50 Lakhs to ₹1 Crore: A strict 10% surcharge is levied directly on your base tax liability.

- ₹1 Crore to ₹2 Crores: An escalated 15% surcharge applies to your base tax calculation.

- ₹2 Crores to ₹5 Crores: The surcharge scales up to 25% for high-net-worth individuals.

- Above ₹5 Crores: The peak surcharge rate reaches 37% for top-tier earners.

Because the initial deductor does not factor in your external wealth, this discrepancy creates a significant funding gap. Non-resident players face an even more aggressive framework, which you can analyze in our guide on NRI Lottery Winnings Tax in India.

Advance Tax Mandates and Section 234 Interest Penalties

Relying on year-end reconciliations to pay off your residual tax gap is an expensive mistake. The income tax framework enforces strict quarterly payment schedules that apply to all forms of taxable income.

Under Section 208, any taxpayer whose residual tax liability exceeds ₹10,000 after subtracting TDS credits must pay Advance Tax. Because a lottery win occurs as a sudden windfall event, it instantly triggers these advance compliance rules.

Failing to meet these quarterly milestones causes the e-filing portal to automatically assess compounding interest penalties when you submit your return. Specifically, Section 234B and Section 234C interest charges accrue at 1% per month for delayed or skipped payments. To ensure full alignment with updated electronic payment formats and deadlines, always cross-reference your schedules with the Official Income Tax Department Portal.

Compliance Protocols After Crossing the Lottery TDS 10000 Threshold

Recovering or declaring funds correctly requires following a precise, sequential filing routine to ensure your records match perfectly across all government ledgers.

Step 1: Verify the TDS deductions reflected inside your Form 26AS ledger.

Step 2: Cross-reference the payout values with your Annual Information Statement (AIS).

Step 3: Declare the gross windfall under Schedule OS (Income from Other Sources).

Step 4: Compute the residual surcharge gap and pay any outstanding balance.

If you notice any discrepancies between your physical Form 16A certificate and your digital Form 26AS ledger, contact the clearing house immediately. The tax department logs data automatically, and any mismatch will stall your return processing or trigger an automated under-reporting audit notice.

Frequently Asked Questions

What is the lottery tds 10000 threshold in India?

The lottery tds 10000 threshold is the legal limit above which prize distributors must deduct tax at source. If a single windfall payout exceeds ₹10,000, a flat 30% base tax plus a 4% cess is withheld before the net funds are released.

Does the 31.2% TDS deduction clear my final tax bill?

No, the 31.2% TDS deduction only covers your baseline liability. If your total annual income from all sources exceeds ₹50 Lakhs, progressive surcharges kick in. This creates an additional tax shortfall that you must clear manually.

Am I required to pay advance tax if my prize faced TDS?

Yes, you must pay advance tax if your remaining tax liability exceeds ₹10,000 after subtracting your TDS credits. You must calculate your additional surcharge or cess gap and pay it during the quarterly tax cycles to avoid penalties.

What happens if I win a prize below the 10,000 threshold?

If you win a prize below the ₹10,000 threshold, no tax is deducted at the source. However, the winnings remain fully taxable. You are legally required to declare the gross amount in your annual return and pay the flat 31.2% tax rate.

Conclusion & Next Steps

In summary, understanding the lottery tds 10000 threshold is only the first step in managing a windfall. While this limit dictates whether tax is deducted upfront, your total annual income ultimately determines your true tax bill.

Therefore, do not leave your compliance to chance. Review your Form 26AS and AIS ledgers immediately after a win, calculate your final surcharge brackets, and clear any outstanding tax balances through the advance tax portal to avoid costly interest penalties.